TrendForce:China Consumes US$10.2 Billion and US$6.3 Billion Worth of DRAM and NAND Flash Chips in 2014

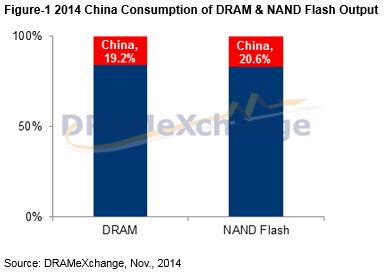

China's GDP showed tremendous growth over the years thanks to the country's positive market developments and economic policies. The business potential of the country's massive consumer market also grew as PC, smartphone, and tablet manufacturers began setting their sights on the country. As of this year, nearly 4.789 billion DRAM chips and 3.518 billion NAND Flash chips from the 2Gb category have been consumed in the China market, accounting for a respective 19.2% and 20.6% of the world's total DRAM and NAND Flash output, according to the latest report from DRAMeXchange, a research division of Taiwan-based market intelligence firm TrendForce.

China's PC DRAM consumption is currently at approximately 15%. Benefiting from domestic demand, Lenovo has managed to raise the scale of its business operations over the years, and is currently acquiring other companies as a means to boost its presence among first tier manufacturers. While the company is still competing fiercely with HP for top position in the PC market, its overall PC shipments are already ahead of all of its other competitors'. For 2015, DRAMeXchange predicts that Lenovo's market share will arrive at approximately 17%. As has been the case with the other markets, Mobile DRAM is expected to gradually replace PC DRAM as the mainstream in China given the country's growing smartphone and tablet sales. Aside from ZTE and Huawei, which are doing relatively well overseas, most China-based smartphone brands are expected to place their focus on the domestic market. Based on TrendForce's 2014 market statistics, China alone already accounts for 28% of Mobile DRAM's overall bit demand. The importance of China's economic development to the entire DRAM industry is expected to become more apparent next year as that proportion rises to over 40%.

As the NAND Flash manufacturing processes are currently advancing to under 1ynm, many NAND Flash applications including smartphone and tablet-based eMMCs and Notebook-based SSDs are showing improved growth in the market. Competition among global OEM manufacturers, meanwhile, is starting to become more intense, with brands other than Apple and Samsung starting to make their way into the country's lucrative market. The level of China's NAND Flash consumption has managed to grow considerably over recent years due to Lenovo's rise to prominence, the above-average growth shown by China's emerging brands, and the improving standards of China's hardware designs. By the end of 2014, DRAMeXchange projects that the NAND Flash market's total value in China will reach up to US$ 6.3 billion. The proportion of China's overall NAND Flash usage relative to the world's NAND Flash output, on the other hand, is expected to hit 20.6% in 2014, and 30% or more in 2015.

China to implement a series of key policies to sustain domestic growth

China's efforts over the years to transform from a manufacturing-based to consumption-based economy has been largely successful. Given the consistent growth in its economy and the country's rising wage levels, many of the productions in China are bound to be outsourced to other emerging countries. The Chinese government's current goal is to improve the country's outlook by implementing strategic policies that are aimed at enhancing its industrial capabilities. One such policy involves increasing the imports of semiconductor components such as smartphone CPU, AP, DRAM, and NAND Flash, the combined value of which exceeds the value of China's imports for oil. In the future, it would be interesting to see whether UNIS’s (Unisplendour Corporation Limited) efforts to integrate resources from Spreadtrum Communications, RDA, and Intel will be successful.

Due to the relatively high proportion of CPU, DRAM, and NAND Flash components imported by China, the government policies that are implemented with regard to these three product categories may prove critical to the country’s industries. A few days ago, the Chinese government announced a policy worth NT$600 billion that involves mastering the technologies at the upper streams of the country's semiconductor supply chain and applying these technologies to mid to lower streams. The main purpose behind this is to enable the country's supply chains to be more integrated and to allow momentum in China’s domestic industries to persist.