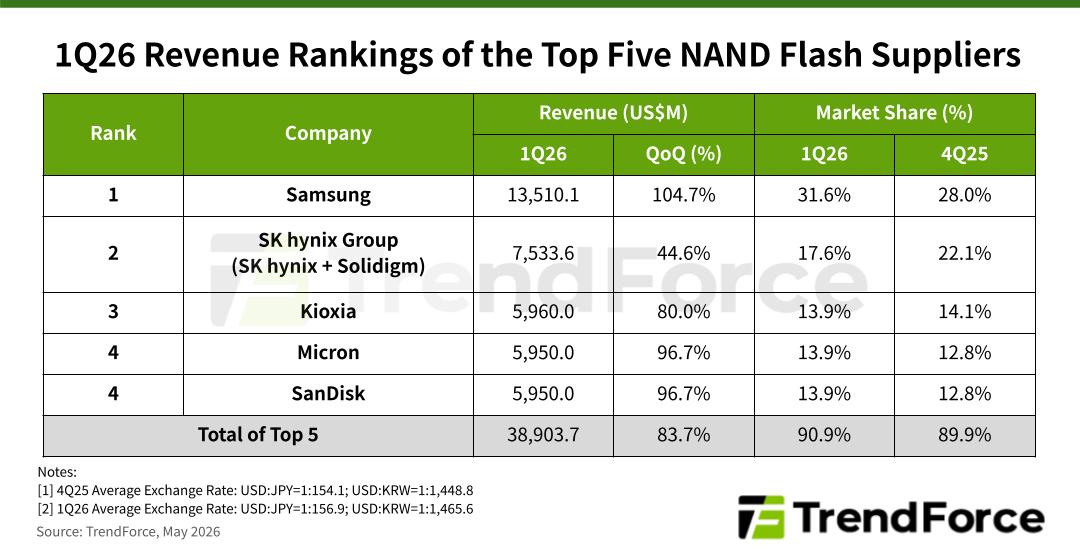

Combined Revenue of Top Five Global NAND Flash Suppliers Rose by 83.7% QoQ for 1Q26 as Supply Shortages Drove Price Hikes

According to TrendForce’s latest survey of the NAND Flash industry, CSPs worldwide experienced an exponential surge in demand for enterprise SSDs in 1Q26 due to the need for high-speed data transmission and the massive data storage capacities required to build out AI server infrastructure. Additionally, a persistent structural shortage of traditional HDDs has led a significant volume of storage-related orders to shift toward QLC enterprise SSDs. Amidst this soaring demand and constrained supply, NAND Flash suppliers’ ASPs broadly exceeded expectations. Hence, the combined revenue of the world’s top five NAND Flash suppliers jumped 83.7% QoQ, surpassing US$38.9 billion.

Moving into 2Q26, the supply-demand imbalance is expected to persist. Although rising memory costs and higher end-product prices have dampened smartphone and PC demand, brisk server orders will fill this gap. NAND Flash suppliers generally anticipate continued growth in their shipments through the second quarter, and their pricing strategies are expected to sustain elevated ASPs.

Looking at individual suppliers’ performances in 1Q26, Samsung firmly maintained its top position in the revenue rankings. The company capitalized on quarterly contract pricing and a significant increase in server-related bit shipments, which drove a substantial rise in its ASP. Consequently, Samsung posted US$13.51 billion in NAND Flash revenue, marking a staggering 104.7% QoQ increase—the highest growth rate among the top five—while expanding its revenue market share from 28% to 31.6%.

SK hynix Group (which includes SK hynix and Solidigm) secured second place with about US$7.53 billion in revenue, reflecting a 44.6% QoQ increase and bringing its market share to 17.6%. This growth momentum was similarly fueled by soaring ASPs. Additionally, the group’s overall revenue was significantly bolstered by its subsidiary, Solidigm, which benefited from a steady influx of orders for high-capacity QLC enterprise SSDs.

Kioxia delivered a strong performance in 1Q26, with revenue climbed 80% QoQ to US$5.96 billion. The company retained its third-place ranking with a 13.9% market share. Buoyed by the overarching surge in NAND Flash prices and highly favorable market dynamics, Kioxia achieved outstanding results in both revenue and profitability.

Micron also benefited from the considerable hike in its NAND Flash ASP. Its 1Q26 NAND Flash revenue jumped 96.7% QoQ to US$5.95 billion, allowing its market share to rebound to 13.9% and tying with SanDisk for fourth place.

SanDisk experienced a massive QoQ revenue increase of over 200% in its data center business, underscoring the success of its strategy to pivot its product mix toward high-value offerings. Its overall 1Q26 NAND Flash revenue matched Micron’s at US$5.95 billion, also reflecting a 96.7% QoQ growth and a 13.9% market share.

TrendForce indicates that major NAND Flash suppliers will add virtually no new production capacity in 2026. Due to persistently strong AI-related demand, supply shortages are expected to last throughout the year. By year-end, NAND Flash products featuring 200 layers or more will firmly establish themselves as the undisputed market mainstream. Furthermore, production resources will remain heavily focused on server storage applications, continuing to drive the market penetration of high-capacity QLC enterprise SSDs.