Consumer DRAM Shortages Extend to DDR2 Products with Contract Prices Expected to Continue Rising in 3Q26

TrendForce’s latest research reveals that structural tightening in mature-node DRAM supply is forcing consumer DRAM buyers to adopt legacy memory products to secure larger supply allocations. This has triggered a new wave of demand for procuring older-generation DRAM components, driving continued price momentum across legacy products such as DDR2 and DDR3.

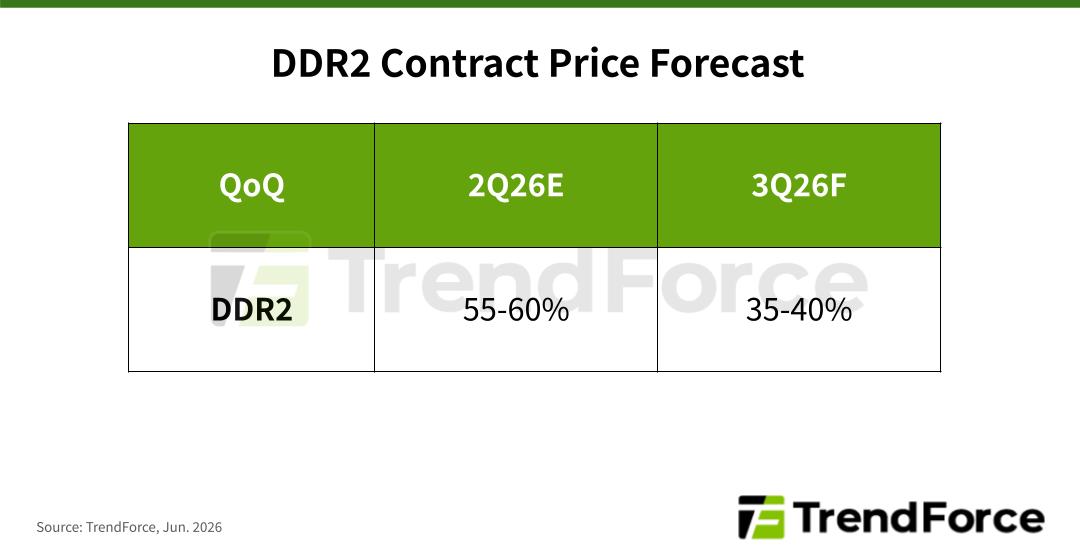

Following strong gains in 1Q26, TrendForce estimates DDR2 contract prices will rise by approximately 55–60% in 2Q26, followed by a further 35–40% increase in 3Q26.

TrendForce notes that on the supply side, the three major DRAM suppliers continue to prioritize advanced-node production to support growing demand for HBM and server DRAM driven by AI infrastructure investments. As a result, wafer allocations for DDR4 and other mature-node products have been reduced, forcing buyers of consumer DRAM, such as DDR4, to seek support from Taiwanese DRAM suppliers.

Companies such as Nanya and Winbond have gained substantial pricing leverage as demand significantly exceeds the bit output available from Taiwanese vendors. Given limited supply, these suppliers have strategically reduced production of lower-margin products and shifted capacity toward higher-value offerings to improve profitability.

Continued shortages of consumer DRAM components and rapidly rising contract prices have prompted some OEMs and ODMs to downgrade memory specifications to control system costs. In some cases, DDR4 designs are being replaced with DDR3 solutions, while certain DDR3-based products are being redesigned to use DDR2.

Customers are aiming to secure more reliable supply allocations by adopting lower-capacity configurations or older memory generations. Consequently, supply shortages in consumer DRAM are cascading down through successive technology generations.

Winbond gradually exits DDR2 production while ESMT expands capacity

Key suppliers of DDR2 components include Winbond and ESMT. However, Winbond is gradually reducing DDR2 production and reallocating capacity toward higher-margin products such as DDR3, DDR4, and LPDDR4. This transition is expected to tighten DDR2 supply conditions further.

In contrast, ESMT plans to maximize DDR2 production within its existing wafer allocation at PSMC, concentrating resources on this segment to enhance profitability and help offset the supply gap created by Winbond’s withdrawal from the DDR2 market.