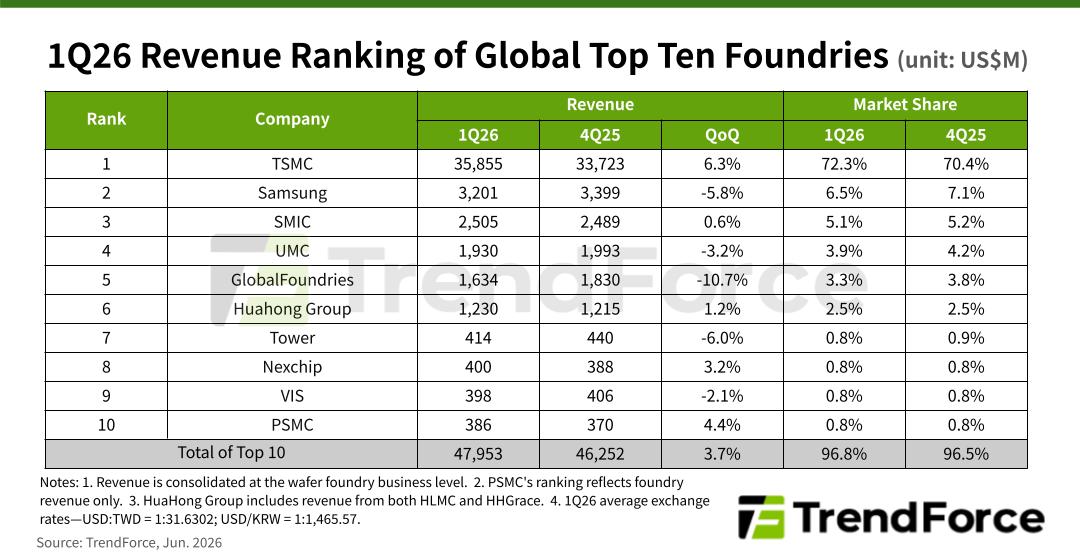

Strong AI Demand and Early Consumer Electronics Inventory Build Drive Top 10 Foundries to 3.7% QoQ Revenue Growth in 1Q26, Says TrendForce

TrendForce's latest investigation into the foundry industry reveals that strong shipments of AI HPC chips and related components continued throughout 1Q26. Meanwhile, TV and PC/notebook supply chains accelerated production schedules and increased inventory levels for peripheral ICs, prompting foundries to receive pull-in orders and additional customer bookings.

Although smartphone seasonality remained a headwind, the impact was largely offset by early inventory replenishment across consumer electronics supply chains. As a result, the traditional seasonal slowdown was notably muted, with combined revenue of the world's top 10 foundries rising 3.7% QoQ to US$47.95 billion, setting another quarterly record.

Looking ahead to 2Q26, TrendForce expects the benefits from early inventory stocking by TV and PC/notebook ODMs and brands to extend for roughly another quarter. Additionally, smartphone vendors are gradually entering their new product build cycle.

Foundries are starting to hint at possible wafer price increases in the second half of 2026 as utilization rates improve, causing some process nodes to reach their lowest point and start recovering in price. This development is likely to encourage customers to place orders early in anticipation of upcoming price rises.

Demand for AI-related advanced-node production and power-management products continues to exceed expectations, creating both order spillover effects and capacity crowding across the industry. TrendForce forecasts that revenue for the world's top 10 foundries will reach another record high in 2Q26, with sequential growth accelerating from the previous quarter.

TSMC benefited from sustained demand for AI server GPUs and xPUs during the quarter. Growing deployment of Agentic AI and general-purpose servers also drove strong demand for server CPUs. The company’s revenue increased 6.3% QoQ to nearly $35.86 billion, demonstrating resilience despite the seasonal downturn. Market share expanded further to 72%, even during what is typically a weaker quarter.

Samsung Foundry (excluding System LSI) also received some pull-in orders from TV and PC/notebook supply chains. However, these gains were largely offset by smartphone seasonality. Revenue declined 5.8% QoQ to slightly over $3.2 billion, while market share slipped to 6.5%. Samsung nevertheless maintained its position as the world's second-largest foundry.

SMIC received pull-in orders from TV brands and PC/notebook ODM customers during the quarter. Furthermore, wafer price increases negotiated with some 8-inch customers in 2H25 began taking effect. Both wafer shipments and ASPs recorded modest sequential gains, lifting revenue 0.6% QoQ to $2.51 billion. Market share remained stable at 5.1%, securing its third-place ranking.

UMC also benefited from inventory-building activities across TV and PC/notebook supply chains, receiving additional orders from both 8-inch and 12-inch peripheral IC customers. Capacity utilization and wafer shipments improved sequentially. However, a higher proportion of 8-inch wafer shipments reduced ASPs by approximately 5%, resulting in a 3.2% QoQ decline in revenue to $1.93 billion. UMC maintained fourth place with a 3.9% market share.

GlobalFoundries saw fewer benefits from consumer electronics inventory replenishment due to its customer mix and was also affected by seasonal weakness in smartphone-related peripheral IC demand. Both wafer shipments and ASPs declined during the quarter, causing revenue to fall approximately 11% QoQ to just over $1.63 billion. Market share slipped slightly to 3.3%, though the company retained its fifth-place position.

TV and notebook supply chain pull-ins reshuffle rankings, pushing Nexchip to a record-high eighth place in 1Q26

HuaHong Group’s subsidiary, HHGrace, recorded modest wafer shipment growth that was largely offset by ASP declines, resulting in revenue remaining broadly stable. Including HLMC, HuaHong Group's consolidated revenue increased 1.2% QoQ to $1.23 billion, maintaining a 2.5% market share and sixth-place ranking.

Tower Semiconductor was affected by seasonal weakness in consumer electronics peripheral IC demand, with revenue declining 6% QoQ to $414 million. The company maintained seventh place with a market share of 0.8%.

The inventory build cycle across TV and PC/notebook supply chains led to another reshuffling among the eighth- to tenth-ranked foundries. Nexchip, whose customer portfolio is heavily exposed to TV and PC/notebook peripheral ICs, benefited more significantly than its peers from the pull-in effect. Revenue increased 3.2% QoQ to $400 million, allowing Nexchip to climb from ninth place in the previous quarter to eighth—its highest ranking on record.

VIS benefited from urgent pull-in orders for PC/notebook and TV large-display driver ICs (LDDICs), as well as steady demand for smartphone and AI-related PMICs. Although wafer shipments and utilization rates improved sequentially, the higher mix of DDIC shipments weighed on ASPs, resulting in a 2.1% QoQ decline in revenue to nearly $400 million. VIS ranked ninth with a market share of 0.8%.

PSMC continued to benefit from rising memory prices. Excluding memory operations and considering foundry revenue only (memory and logic foundry services), revenue increased 4.4% QoQ to $386 million, securing tenth place with a market share of 0.8%.